Glencore posts lower metals output for first nine months, reiterates outlook

The miner and trader's own sourced copper production fell 4% to 705,200 metric tons, while its own sourced cobalt output fell 18% to 26,500 tons.

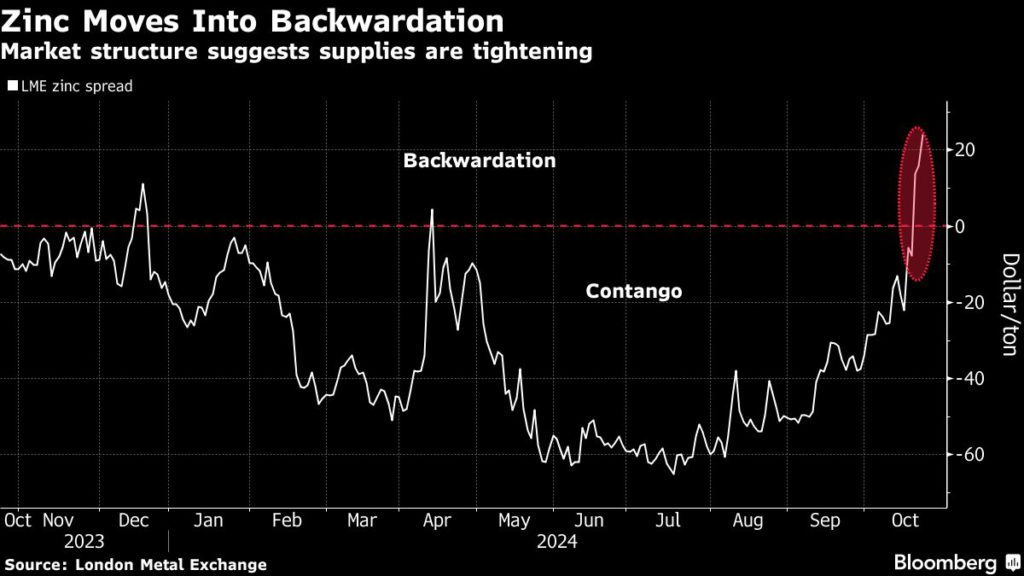

Spot zinc prices have shot above later-dated futures on the London Metal Exchange, signaling a tight market as large buyers scoop up inventories and pile into futures at a time when a string of mine disruptions threatens to throttle supplies.

Cash zinc contracts are trading at a $24.09 premium to three-month futures, in a pricing structure known as backwardation that’s a hallmark sign that spot demand is exceeding supply. The spread was trading at a discount as recently as last week, and is now at the highest level since 2023.

The zinc market has been rattled by a series of mine setbacks this year, dramatically tightening supplies of raw zinc ores known as concentrates. Demand for the metal has suffered during an industrial downturn in China and Europe, but the supply ructions have been large enough to underpin an 17% gain in zinc prices on the LME this year.

The key question among analysts and traders is whether zinc smelters — squeezed by rising raw material costs and weak end-use demand — will be forced to cut production. That could constrict spot metal supplies and fuel further price gains. The backwardation signals that buyers in the LME market are increasingly alert to that possibility.

Within the past week, one individual buyer has acquired between 50% and 80% of the readily available zinc inventories in the LME’s warehousing network, according to data from the exchange. And in the futures market, one entity has also bought up at least 40% of the main November-delivery zinc contracts, which would entitle them to scoop up more inventory than there is available in the system, if held to expiry.

“Has this tightness been accentuated by changes in trader positioning? Maybe, but there’s a fundamental basis for it because we’re simply not mining enough zinc,” Colin Hamilton, managing director for commodities research at BMO Capital Markets, said by phone from London. “I can see why it’s happening, because on the raw-material side it’s the tightest of all the base metals.”

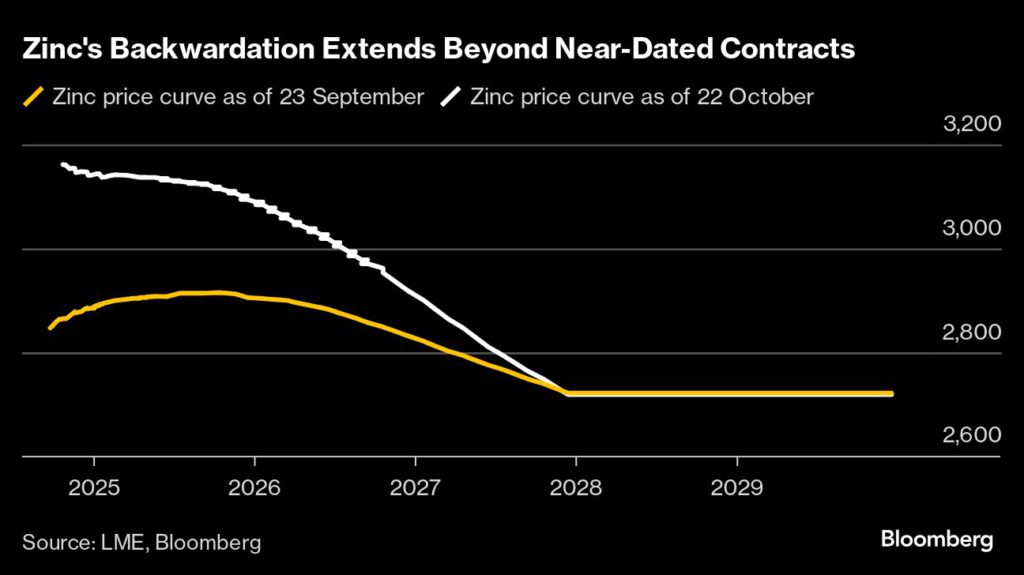

Backwardations can emerge quickly in individual price spreads as large buyers emerge on the LME, and they can dissipate just as rapidly if and when those inventories and futures positions are sold back into the market. But the tightness isn’t limited to near-dated months, with a steep backwardation emerging all the way out to 2027 in recent trading sessions — suggesting that investors, traders and consumers could be bracing for a longer-term squeeze on supply.

Global mine production fell by 4.2% in the first eight months of the year, data from the International Lead and Zinc Study Group showed on Wednesday. Meanwhile, refined zinc output has fallen 1%, but BMO’s Hamilton said it’s likely that more meaningful smelter cutbacks will be seen moving into next year.

Bullish investors have been betting on a slower-than-expected recovery in mined supplies following a series of cuts to production guidance, including a downward revision by Ivanhoe Mines Ltd. earlier this month, according to Zeng Tong, an analyst at Jinrui Futures Co.

The latest knock to mine supply came on Friday, as Sibanye Stillwater Ltd. said that it expects operations at its Century zinc mine in Australia to be suspended until mid-November after a bushfire damaged some equipment.

Investors might be rushing to build long positions following the Century news, said Han Zhen, an analyst at researcher Shanghai Metals Market. There is also talk about possible production cuts at European smelters due to higher electricity costs over winter, she said.

Zinc was down 0.4% at $3,126 a ton on the LME as of 1:32 p.m. in London, after climbing 2% on Tuesday. Other metals were mixed, with copper down 1.2% to $9,470 a ton, while aluminum rose 0,3%.

Column: Zinc facing supply deficit as mine output falls again

Comments